FAQ topics

Scheme staging dates

Scheme connections to the ecosystem

Dashboards launch date

Multiple dashboards

Dashboards display standards

Digital identity verification

Personal data matching

Pension amount data

State pension

Tax

Scheme members’ next steps

Pension data export

FAQs last updated: 11 April 2022

SCHEME STAGING DATES

Q. Must all pension schemes connect to the pensions dashboards ecosystem, and if so, when?

A. All schemes, across both the public and private sectors, must connect to the dashboards ecosystem. DWP has allocated each scheme a statutory dashboards staging deadline date by when they must have connected. For schemes with 100 or more active and deferred members (in total), these staging dates are spread across a 30-month period from April 2023 to October 2025. Schemes with less than 100 actives and deferreds are expected to stage from 2026 onwards, but DWP has not yet allocated staging dates for these schemes.

Q. Where can I find out our scheme’s dashboards staging date?

A. Schemes’ dashboards staging dates are shown in Schedule 2 of the draft Pensions Dashboards Regulations 2022 which were published by DWP in January 2022. DWP are expected to publish final regulations later in 2022. A handy summary of the draft staging dates is available on the back of the PLSA Pensions Dashboards Pension Scheme Checklist.

The Pensions Regulator (TPR) will be writing to the Chair of Trustees of each scheme with an official “12 months’ notice of your staging date” letter, and further information is expected to be published on TPR’s website in due course.

SCHEME CONNECTIONS TO THE ECOSYSTEM

Q. Will our scheme administrator connect our scheme to the ecosystem?

A. It is likely that many third-party administration (TPA) firms will offer a new service to their scheme clients to connect them to the dashboards ecosystem. Schemes should be discussing this with their TPAs now. In-house administered schemes should be discussing their options with their technology providers. Schemes may also wish to consider if they should review alternative Integrated Service Provider (ISP) connection options – for definitions, such as ISP, please see the Pensions Dashboards Programme (PDP) Glossary.

DASHBOARDS LAUNCH DATE

Q. When will pensions dashboards be made available to the public?

A. Even though pension schemes will be connecting to the ecosystem from April 2023 onwards, that isn’t when dashboards will be launched to the public. The date when dashboards will be made available, or the Dashboards Available Point (or DAP), has not yet been defined. At the PLSA, our view is that there should be many months of live “private beta” testing from April 2023 onwards, before the Full DAP happens – read more about this in our March 2022 press release.

MULTIPLE DASHBOARDS

Q. Why has the Government decided to make dashboards available in lots of different places, rather than just one 'Government dashboard'?

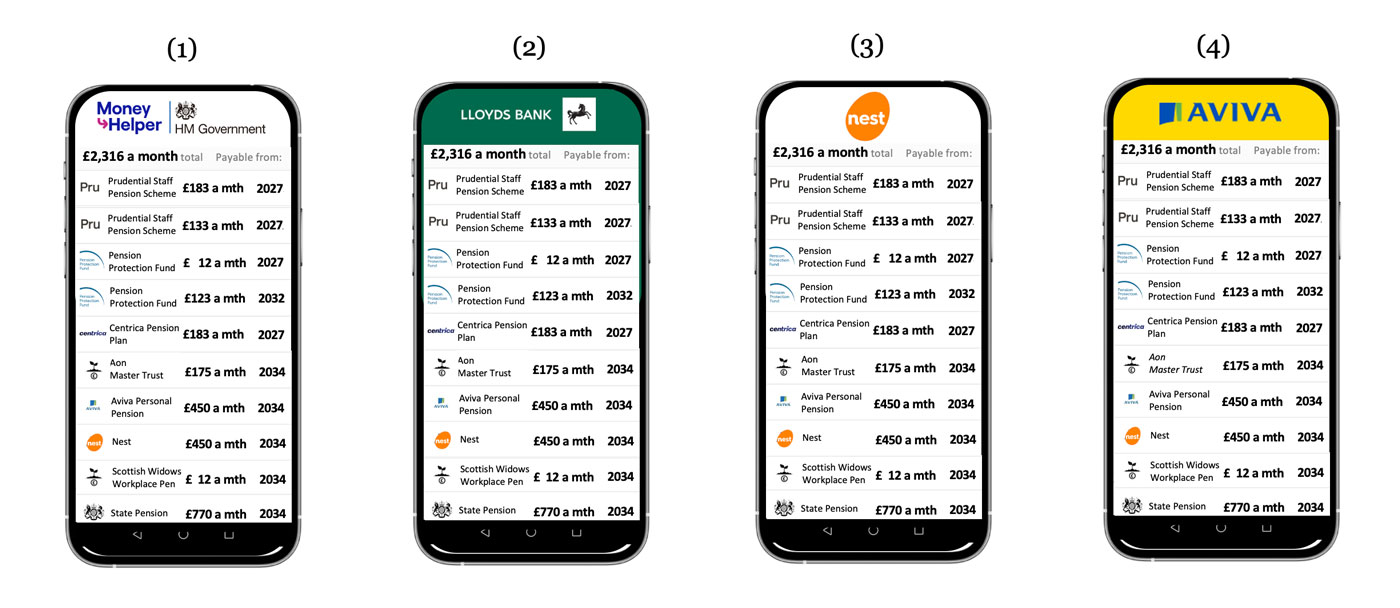

A. The Government wants people to be able to see their pensions together in whatever place they are already comfortable, such as their online banking app, their pension providers’ websites, or elsewhere. But to limit confusion, the Government is also mandating that, all dashboards must display identical data in an identical layout. The best way to illustrate this is through an example.

Below are the real pensions of the PLSA Pensions Dashboards Consultant, Richard Smith. Richard could either see his pensions on the Government’s MoneyHelper dashboard (1), or, if these organisations choose to offer an authorised dashboard service to their members / customers, on the app of his bank (2) or one of his pension providers (3) and (4).

Note: The above are merely concept designs - the PDP Design Standards (see below) will define what dashboards will actually look like. Also note that the Pension Protection Fund (PPF) is currently out of scope for display on pensions dashboards

The Government feels this will maximise the likelihood of Richard (and everyone) seeing their pensions, as they will be available to be viewed in many different places. But the critical point is that the display will be the same wherever you view your pensions.

Q. Will people be able to use more than one dashboard?

A. Absolutely. If they’re in their banking app one day, they could choose to look at their pensions there. Another time, for example, if they’re on one of their pension providers’ websites, then they could look at their pensions there. But what they will see will be the same, wherever they view their pensions.

Q. Will schemes have to connect to more than one dashboard?

A. No, that’s not how Government has designed the ecosystem. All schemes must connect to the Government’s central digital service, and then all authorised dashboards will also connect into this. The central service acts as a sort of ‘switchboard’, receiving Find requests from dashboards, and then securely passing these out to all connected schemes. Watch the 90-second PDP Data Standards video for a graphical explanation of how this will work.

Q. Which dashboard should trustees direct their members to?

A. Action 10 on the PLSA Pensions Dashboards Pension Scheme Checklist encourages trustees to think about this important question, as well as wider communication issues.

Trustees could, for example, direct their members to a particular dashboard*. Or their could signpost a number of dashboards. Or the Government MoneyHelper dashboard. Or some combination of these. You could consider surveying your deferred and active members to ask them where they would like and expect to view all their pensions together.

* remembering that the eventual full list of Qualifying Pensions Dashboards Services (QPDS) will likely be longer than just the three alpha participants of Aviva, Bud and Moneyhub.

Remember too that many, probably most, of your deferred members, also have active pensions elsewhere. The providers of those pensions could well be offering them an authorised dashboard service where they will be able to see their pensions together, including the pension they have with you in your scheme.

Some large schemes, such as Master Trusts, might wish to consider offering their members an authorised dashboard service within their own website or member app. But this is a choice; schemes do not have to offer a dashboard service. Schemes can continue showing just their own scheme’s pension. But, in a dashboards world, you may wish to consider the attractiveness of a scheme website that shows just one pension, when your deferred and active members can go elsewhere to see a summary of all their pensions.

The Netherlands launched their pensions dashboard (MijnPensioenOverzicht.nl or My Pension Overview, known as MPO) over a decade ago. Official Dutch Government research published in 2020 shows that MPO has now become the main place that Dutch citizens go for pensions information, precisely because it shows all their pensions together.

DASHBOARD DISPLAY STANDARDS

Q. Is there scope for dashboards to change how pension information is presented?

A. The PDP Design Standards will dictate what latitude different dashboards providers have to alter the display of information. In January 2022, PDP published an outline set of dashboards Design Standards but the full Standards are due to be consulted on over the summer of 2022. The latitude for display differences may be quite limited, to ensure people see broadly the same thing whichever dashboard they use. More information will be published here once the full PDP Design Standards are published later in 2022.

Q. Will all dashboards use the same standard forecast assumptions?

A. Yes, there will be standard forecast assumptions, but these will be used in forecast calculations done by schemes / administrators and providers (see PENSION AMOUNT DATA below). In terms of dashboards, it’s important to understand that dashboards are not permitted to carry out any calculations at all. Every pension figure shown on all dashboards will have been provided by schemes. There may be very minor exceptions (to be confirmed in the PDP Design Standards) such as dividing annual pension incomes by 12 to show a monthly amount.

Q. How will dashboards’ displays, and the PDP Design Standards with which they must comply, be user-tested with the general public, to ensure they work with people who generally have very low levels of pensions understanding?

A. Considerable user testing has already been done with members of the public. For example, PDP published a detailed User Research Report in January 2022. This user testing is continuing, and being extended, as part of the current alpha development phase. The findings will be used to inform the PDP Design Standards in the Summer of 2022. User testing will continue as schemes connect in 2023, to ensure people of all different types are able to use dashboards effectively and are understanding what they are seeing.

Q. Will target retirement incomes, such as the PLSA Retirement Living Standards, be shown on dashboards?

A. At PLSA, we are strong advocates of the PLSA Retirement Living Standards (RLS) being included on dashboards. Research shows that people need help understanding what total retirement income they could, or should, be aiming for. As with all aspects of dashboards displays, the PDP Design Standards (in the Summer of 2022) will determine whether inclusion of the RLSs is allowed, but they may not go as far as mandating their inclusion.

DIGITAL IDENTITY VERIFICATION

Q. If a fraudster manages to view someone’s pensions on a dashboard, how can trustees ensure that anybody subsequently contacting them has not viewed the member’s pension information in this way?

A: There are two parts to this question. Firstly, a strong central identity verification service is a core component of the dashboards ecosystem, so a fraudster is unlikely to be able to see someone else’s pension information unless the user shares their log in / ID verification details with them, or if the user logs in whilst the fraudster is also looking on.

Secondly, when anyone contacts a scheme, trustees should ensure their administrator’s normal strong identity verification checks continue. For example, this might be by asking the individual something that only the member would know (and which isn’t sent to dashboards), such as the date / amount of their last contribution.

Q. If you have logged in to, say, an online banking app which provides a dashboard service, why do you then need to verify yourself again through the central identity service (which could be annoying for many people)?

A. Verifying your identity to your bank, or pension provider, is not the same thing as verifying it to all pension schemes. This is why the Government has designed the dashboards ecosystem to include a central identity verification service. The alpha and beta testing phases will aim to make this user journey as smooth as possible, but a strong identity process is essential for the protection of individuals (see question above) – see the Identity service page on the PDP website for more details. This PDP page also explains how the Government is developing a UK Digital Identity and Attributes Trust (DIAT) framework which could make it an even smoother process in the future.

PERSONAL DATA MATCHING

Q. Will a scheme only return data if it matches both your NI Number and other elements of personal data? Which elements?

A. Yes, that’s exactly right. For every Find request schemes receive from the central Government service, they must compare their records against certain personal data elements on all of their members’ records to see if they have a match. Working with their administrator, it is up to each scheme’s trustees to determine which particular personal data elements they should compare against. See the PASA Data Matching Convention (DMC) Guidance for more details on this.

Q. Might there be a temptation for schemes to err on the side of not returning data, because the legal risks of returning 'wrong' data are presumably higher than they are for saying simply 'no match' or 'maybe match'?

A. Yes, this is a possibility. The January 2022 DWP consultation on the draft dashboards regulations set out how trustees “must balance their existing GDPR duties not to disclose an individual’s data to the wrong person with their new dashboard duty to match and return an individual’s data to them”. The PLSA is calling for Guidance from the two respective regulators (Information Commissioners’ Office (ICO) and The Pensions Regulator (TPR)) on how trustees should optimally strike this balance.

Q. What additional checks can schemes carry out to ensure their personal data is accurate at all times?

A. Some TPAs are ramping up their ongoing member verification services, to ensure personal details are up-to-date and accurate on as many of their clients’ members as possible, and thus ensuring they will be able to make positive matches against dashboards Find requests. Schemes should be talking to their TPAs about what they are doing to continually maintain personal data accuracy – see Action 7 on the PLSA Pensions Dashboards Pension Scheme Checklist.

PENSION AMOUNT DATA

Q. How is it possible that all dashboards are able to show the same pension amount data as all other dashboards?

A. When schemes make a positive match against a Find request, they must return a secure flag to the central Government service, which is then passed back to whichever dashboard the individual is using. This flag, in effect, says: “Yes, we have a pension for you”.

The individual can then press a button on that dashboard which makes a View request direct to the scheme(s) where a pension has been found. Those schemes must then return a small, prescribed set of information about the pension they have for the individual.

Once the individual logs out of the dashboard they are using, the data is dropped – no data persists anywhere in the ecosystem. The next time the individual uses a dashboard, a further View request (with the user’s consent) will re-retrieve the pension information direct from the scheme. Of course, this information may be different from the previous View request if the administrator has updated the member’s record between the two View requests.

Q. How quickly must pension amount data be returned?

A. The draft dashboards regulations state that, where it has already been calculated in the last 12 months, pension amount data must be returned immediately. Otherwise, administrators have 3 or 10 working days, for DC and DB amounts respectively, to calculate and return the prescribed pension amount data. The PLSA’s view is that this 3 / 10 working day provision is unhelpful: schemes should either return pension amount data straightaway (where it is already calculated and stored), or the message should be “Contact your scheme for pension figures”. Final regulations are expected later in 2022.

Q. How up to date must the pension amount data be, and what impact will this have on the frequency of data refresh by the administrator?

A. The draft dashboards regulations state that pension amount data must be as at a date within the 12 months prior to the View request.

Many schemes may therefore choose to calculate DB and DC pension income amounts for all deferred and active members as an annual bulk exercise. Many schemes already do this.

Schemes should be discussing with their TPAs / ISPs what an appropriate refresh periodicity is going to be to best meet this requirement.

Q. How will different payable dates be dealt with?

A. Each pension entitlement must be returned with a payable date, usually the scheme’s normal pension date, or the individual’s selected retirement date. There will likely be a range of different dates across an individual’s different pensions. Dashboards will not support any ability to recalculate what the pensions would be if they were all paid from the same date, i.e. at earlier or later payable dates for each pension. For these more detailed figures, individuals should contact their schemes directly.

Q. How will consistent Defined Contribution (DC) pension incomes be calculated?

A. The Financial Reporting Council is currently consulting on changes to standardise the projection basis to be used for all DC pensions, known as the Statutory Money Purchase Illustration (SMPI) Actuarial Standard Technical Memorandum 1 (AS TM 1).

The proposed changes require all DC schemes to adopt standardised future growth assumptions, and standardised assumptions for converting the future projected DC fund into an income. FRC is proposing that this is a non-increasing, single-life annuity.

Q. Will forecast pension incomes be in today’s money?

A. Yes. This is a key component of the DC pension incomes projected on the SMPI basis. And for DB pension incomes, actives’ pension incomes will be based on current earnings and deferreds’ will be revalued to a date within the last 12 months.

STATE PENSION

Q. Will dashboards show the State Pension?

A. Yes, DWP has committed to the State Pension being included on dashboards from the Dashboards Available Point (DAP), i.e. the date from which dashboards are made available to the general public.

TAX

Q. How will the tax treatment of pensions be shown on dashboards?

A. Initial dashboards will provide an indicative summary snapshot of an individual’s pensions, as at dates over the last year. They will not cover any aspects of the tax treatment of pensions. For information on all tax-related matters, such as tax free cash lump sums, the annual and lifetime allowance, and so on, individuals must contact their schemes directly.

SCHEME MEMBERS’ NEXT STEPS

Q. Who should users of dashboards go to with questions about the pension information they see on a dashboard?

A. This will all need to be thoroughly user tested during the beta testing phase, but it is very likely that all questions about the pension amounts themselves would need to be directed to the pension scheme which provided the data. Dashboard providers will undoubtedly receive some queries as well so will need to be ready to deal with them.

Q. If a dashboard user goes to one of their pension providers with a question, will the ecosystem automatically “pass across” the necessary information (such as their pension member number) or will the user have to note it down and provide it to the scheme themselves?

A. Currently, the PDP Data Standards require schemes to return a website address for the scheme / TPA where the individual should go with any queries about their pension information. There is no provision at the moment for the “passing across” of any data, such as pension member number, to the scheme / TPA.

Q. Pensions dashboards will be useful for individuals to see where their different pensions are as well as an indicative summary snapshot of the income each pension might provide in retirement. But how will all the complexities of DB and DC schemes be taken into account?

A. Initial dashboards will not cover all the complexities of DB and DC schemes. For accurate, up-to-date, retirement quotations, including all benefit options, members must still contact their different schemes directly. Early user research is showing that an indicative summary snapshot of the total retirement income they might get is sufficient to meet the needs of many individuals, especially when set against a target income such as the PLSA RLSs.

Q. How are administrators expected to deal with the inevitable increase in admin demand once individuals have used dashboards?

A. TPAs are expecting an increase in requests for definitive figures when dashboards are launched. They may need to increase resources to respond to this increased demand, within the normal disclosure timescales.

PENSION DATA EXPORT

Q. How easy (technically and legally) will it be to export the dashboard data, whether directly via a button or through techniques like screen scraping?

A. DWP asked about data export in their recent dashboards consultation. We await DWP’s response in the summer. PLSA’s response said: “We are not in favour of data being exported in the first iteration of pensions dashboards but are not against this for future iterations”.