PLSA Implementation Statement guidance for trustees

Our guidance and vote reporting templates provide practical support for trustees of both DB and DC/hybrid schemes around the production of their new Implementation Statements, where trustees must disclose how they have followed the objectives and policies set out in their Statement of Investment Principles.

The guidance sets out:

- What the legislation requires and by when

- Some high-level ‘general principles’ for implementation statements

- More detailed possible considerations

- Specific guidance on voting behaviour

- Top tips for investment (and responsible investment) communication.

The guidance includes a specific chapter on how to produce clear, effective and meaningful disclosures on voting behaviour in the Implementation Statement. To help trustees take this next step after reading the guidance and gathering the relevant information, we have also produced templates and guidance for asset owners and asset managers.

The asset owners' voting reporting template and guidance sets out:

- An overview of the template

- Where the template ‘fits in’ as part of the trustees’ broader work to scrutinise their managers’ voting behaviour undertaken on their behalf

- The steps trustees need to take before presenting the template to managers

- What information trustees will get from the template

- How to use this information.

The asset managers' version, also available as an Excel file, contains guidance for asset managers on how to fill out the template, which may also be worthwhile for trustees and their advisers to read.

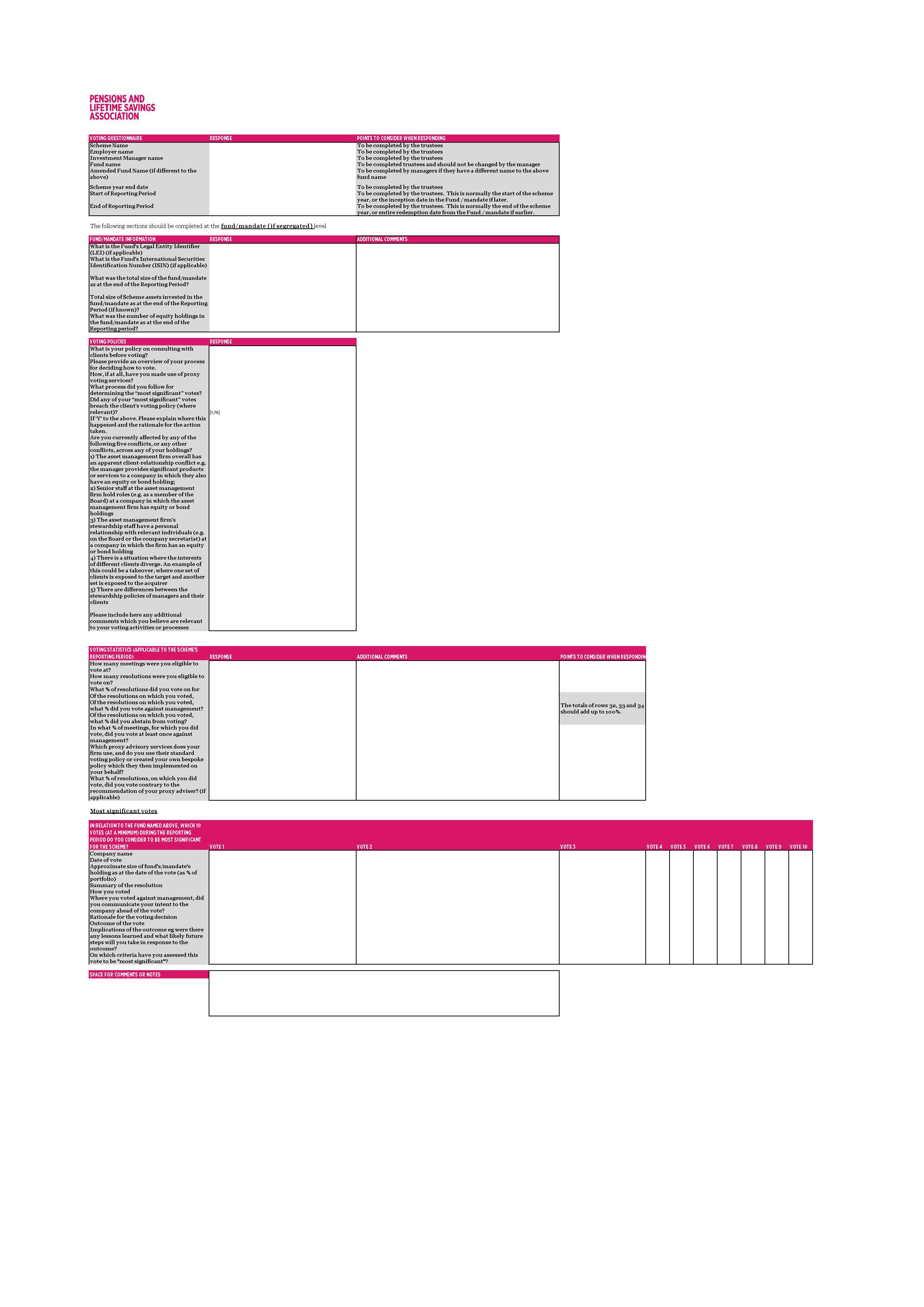

Although the primary purpose of following the guidance should be to ensure voting behaviour is consistent with the trustees’ investment objectives, any significant decisions which are taken by trustees using the structure below could also be used in any descriptions of trustees’ voting behaviour in their Implementation Statements.

Download in the member area

Vote Reporting Template FAQs

Q. Over what reporting period should the templates be completed?

A. The relevant regulatory requirement is that implementation statements include votes cast and engagement activities in the scheme year being reported on. To meet this expectation you should seek, at a minimum, to receive information annually, and in keeping with the scheme year end. This does not however prevent you agreeing more regular reporting schedule with your manager. We would expect trustees and their advisors to regularly engage with managers about obtaining relevant materials to discharge their fiduciary duties, and to ensure that appropriate notice is given to enable the necessary information to be compiled.

Q. What assets should be reported on?

A. The information provided should cover segregated mandates, pooled funds, unit-linked contracts of insurance and other similar products invested by the trustees of the scheme. Contacts of insurance, such as bulk annuities, individual insurance contracts, and other similar products, can be excluded.

Q. What votes should be included in the template?

A. Only votes relating to listed equities – shares traded on regulated markets – are within the scope of the template. Schemes and managers do not need to report on votes relating to debt instruments and private markets.

Q. How should ‘significant votes’ be determined?

A. The PLSA suggests 10 significant votes - in relation to each segregated mandate, pooled fund or unit-linked contract making up any DB scheme section and any DC default fund - should be reported on to enable trustees to meet their own regulatory obligations. It is reasonable for asset managers to set out their view of a ‘significant vote’ in a mandate, as long as a clear and consistent justification for the selections is in place. In heavily concentrated portfolios it would also be reasonable on a ‘comply or explain’ basis to report on fewer votes. However, we would recommend that trustees should also assess those votes and satisfy themselves that this is in keeping with what would be considered significant for their scheme and the agreed mandate.