Don’t gamble savers’ long-term interests for short-term gain by pension tax reform, says NAPF

30 September 2015, Press Release

The National Association of Pension Funds (NAPF) today (Wednesday) published its response to H M Treasury’s consultation ‘Strengthening the incentive to save: a consultation on pensions tax relief’. In it, the NAPF argues clearly that over the long term a move to a pensions tax regime of either ‘taxed, exempt, exempt’ (TEE) or a single rate jeopardises both pension saving and the tax revenues of future governments.

The Chancellor may raise more tax revenue in the short term by a change to pension tax but there is no evidence to show that savers would save more as a result of further changes to the system.

The NAPF shares the Government’s desire to get more people saving more for their retirement but warns there are significant risks associated with a move to either TEE or a single rate. Instead, the NAPF urges the Government to focus its efforts on securing and building on the success of Automatic Enrolment, as we reach the crucial point for millions of small employers who are starting to enrol their employees for the first time.

Joanne Segars, Chief Executive, NAPF, said:

"The Government must be straight with savers, schemes and employers about what it is really trying to achieve with these reforms. It says it wants to incentivise saving but it also wants to increase the revenue to the Exchequer – but these two objectives are incompatible and lead to quite different courses of action. There is a very real risk that to increase the tax take in the short-term the Government will gamble away the long-term interest of savers.

“Our message to the Government is clear – do not act rashly and put at risk the very real success of Automatic Enrolment. Rushing these reforms will be bad news for savers with less money going into their pension pot each month, bad news for schemes with a massive amount of additional administration, bad news for employers with a big bill to pay for all the changes and bad news for the Exchequer with less money being paid in tax in the future.”

A copy of NAPF’s consultation response can be found here and a copy of our earlier press release ‘Pension Taxation Myth Buster’ can be found here.

Why TEE is bad news

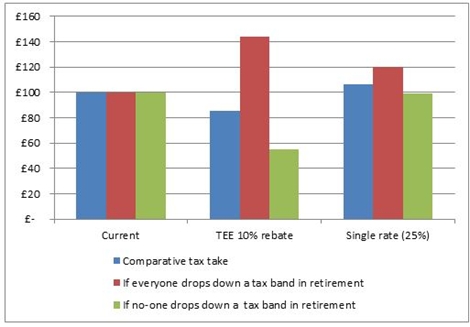

- Modelling a central scenario the tax take for TEE would be 15% less than the tax take under the current system1.

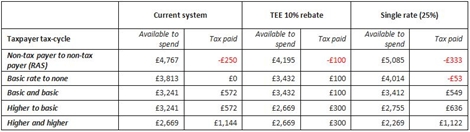

- Non-taxpayers and basic rate savers will lose money in a shift to TEE from the current system2.

- People will need to save more to offset the loss of tax take to future Exchequers and ensure there is no increased pull on State resources from a growing retired population3.

- 82% of our surveyed members believe TEE would reduce pension saving4.

- 63% of our surveyed members say it will add more than 10bp to member charges4.

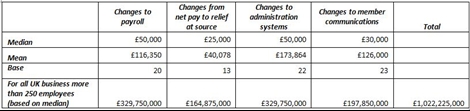

- Additional payroll costs for employers of £20,000 - £800,000 depending on the size of scheme5.

- Additional administration charges estimated at £25,000 - £1million depending on the size of the scheme5.

Why a single rate is bad news

- 86% of the respondents to the survey said they would close their defined benefit scheme (DB) to accrual and move to a defined contribution (DC) scheme4.

- 20% of respondents said they would respond by changing benefits, half of these would replace pension contributions with cash or other benefits4.

- A single rate would have to be set at 25% or lower to meet the Chancellor’s test of sustainability. This brings limited benefit to basic rate tax payers and reduces the attraction of saving in a scheme for higher rate tax payers. If higher rate tax payers leave schemes the costs go up for those left in it (mostly basic rate tax payers).

- All employers will have to change their payroll systems with an average (mean) cost of over £110,000 per scheme5.

ENDS

Notes to editors:

The NAPF is the voice of workplace pensions in the UK. We speak for over 1,300 pension schemes that provide pensions for over 17 million people and have more than £900 billion of assets. We also have 400 members from businesses supporting the pensions sector.

We aim to help everyone get more out of their retirement savings. To do this we spread best practice among our members, challenge regulation where it adds more cost than benefit and promote policies that add value for savers.

NOTE 1: comparative tax revenue in NPV terms (comparing tax revenue for every £100 under the current system to TEE and single rate)

Key assumptions for the above chart:

- Growth rate for funds over 25 years = 6%

- Charges on fund = 0.5% (slightly higher than the average charge made by NAPF schemes but lower than the charge cap)

- Discount rate to arrive at NPV = 3.5% (long term rate used by HM Treasury)

- Central scenario based on mix of taxpayers as per table below (percentage of contributors per tax band based on PPI analysis 2013, the percentage sticking at rate is based on NAPF assumptions).

NOTE 2: Pension savings at retirement and tax contributions by different tax payers, modelled in three pension tax regimes

The tax contributions in the table below are based on £1,000 investment with a gross growth rate of 6%, less charges of 0.5%, invested for 25 years untouched and spent in retirement.

NOTE 3: The wider fiscal picture

Number of tax payers

Source: HMRC, , with projections to 2015-16. Projections: 24.7m basic (83.2%); 4.6m higher (15.6%); and, 332,000 additional (1.1%).

All the charts below are taken from the published by the Office for Budget Responsibility in June this year.

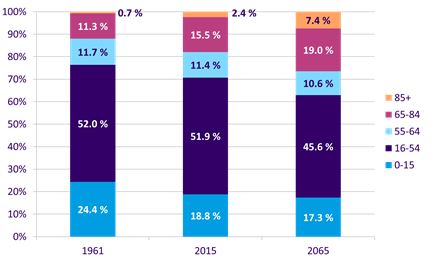

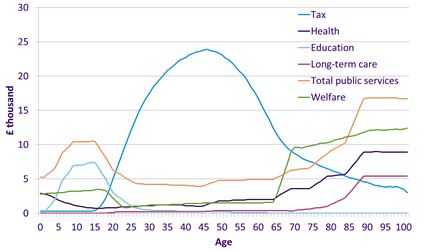

Growth in the UK’s older population

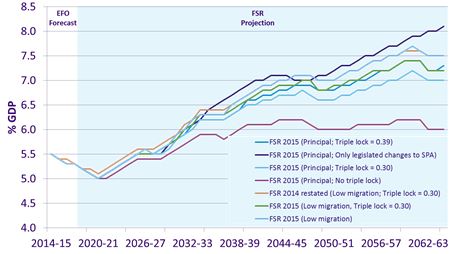

Long term state pension forecast

OBR mapping of Government spending and tax receipts over a lifetime

NOTE 4: NAPF member survey

Survey sent to all NAPF members in September 2015. 93 responses – 75 from fund members and 18 from business members. Not all respondents answered all questions.)

NOTE 5: Estimated costs to schemes of making changes to payroll, administrative and member communications

Source for cost estimates: NAPF member survey September 2015. The figures below based on multiplying the median cost by the number of UK businesses with over 250 employees (6,595) according to BIS Statistical Release of business population estimates for UK and regions 2013.

Contacts:

Lucy Grubb, Head of Media and PR, NAPF, 020 7601 1726 or 07713 073023, [email protected]

Eleanor Bennett, PR Manager, NAPF, 020 7601 1718 or 07825 171 446, [email protected]

Kathryn Mortimer, Press Officer, NAPF, 0207 601 1748 or 07901 007713, [email protected]