Almost 80% in favour of stronger checks to avoid pension scams: PLSA calls for authorisation regime to help stop scammers in their tracks

19 February 2018, Press Release

New research from the Pensions and Lifetime Savings Association (PLSA) highlights the difficulty people have in spotting pension scams and backs stronger checks to help people avoid them. This research builds on the PLSA’s call for an authorisation regime for pension schemes receiving transfers to help stop fraudsters in their tracks.

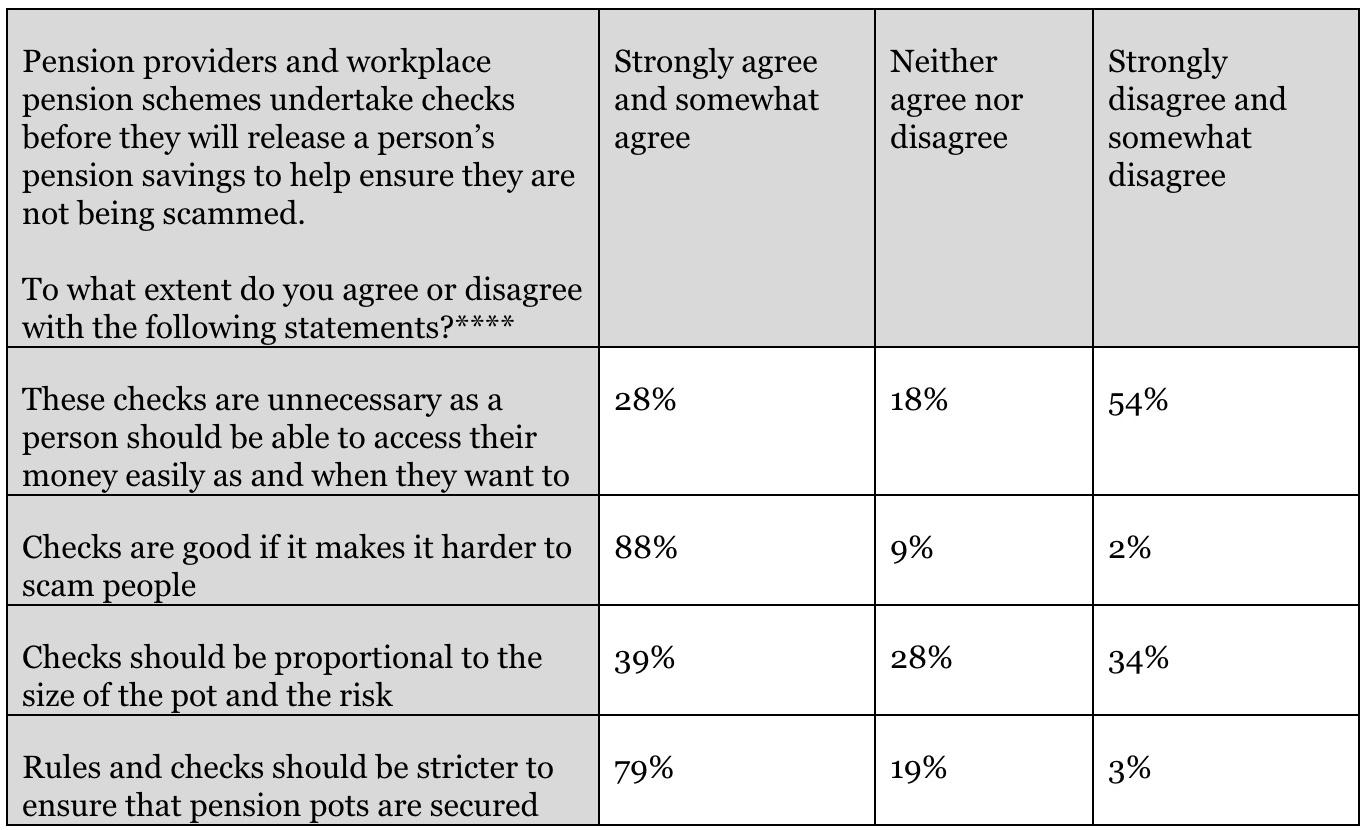

Stronger Checks

Pension scams are an emotive issue and only 8% did not have a view on one of more of the statements about checks. Of those pension savers who did, the majority (88%) agreed the checks that pension providers and workplace pension schemes undertake to help protect against scams were good, as long as they make it harder to scam people.

Four fifths (79%) agreed there should be stricter rules and checks to ensure that pension pots are secured. Only 28% felt these checks are unnecessary because people should be able to access their money easily as and when they want (Table 1).

Consumer Understanding

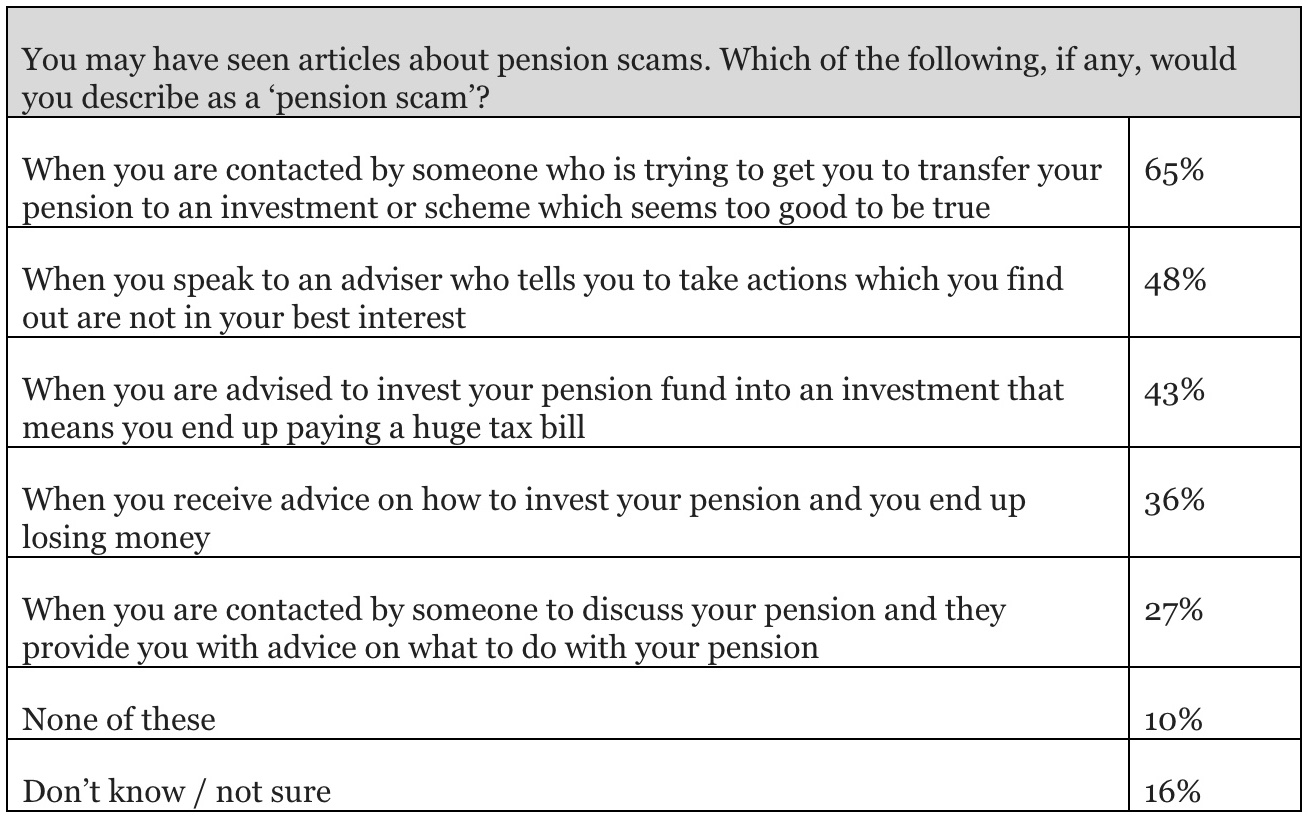

To test people’s understanding of this important topic, the PLSA provided more than 2,000 people with a selection of scenarios that might be pension scams (Table 2). The research found that a worrying proportion (29%* equating to 14.8m UK adults**) missed the most obvious pension scams.

Indeed, the majority (65%) were able to identify a situation “when they were contacted by someone who is trying to get you to transfer your pension to an investment or scheme which seems too good to be true” as a scam but were less sure about other scenarios.

Less than half (48%) of respondents thought that “when you speak to an adviser who tells you to take actions which you find out are not in your best interest” could be a pension scam and only 43% thought “when you are advised to invest your pension fund into an investment that means you end up paying a huge tax bill” described a pension scam.

Most scams seem like they could be legitimate so some respondents were wary about situations which might be completely authentic. Indeed, 36% felt that if “they received advice on how to invest their pension and subsequently lost money” it could be a scam and 27% thought that if “they were contacted by someone to discuss their pension and provided with advice” described a scam.

These findings are concerning given that one in six (17%) of those with a pension say they have been contacted by a company, other than the one that provides their pension, to discuss making changes or transferring their pension. One in ten (11%) have even been contacted multiple times.

James Walsh, Policy Lead for Engagement, EU and Regulation at the PLSA, commented:

“Today’s research shows that consumers struggle to identify pension’s scams and are keen to see stronger checks. As an industry, we need to step up to this challenge and the Government’s recent commitment to tabling an amendment to the Financial Guidance and Claims Bill*** to introduce a ban on pension cold-calling is a step in the right direction. However, pension scams come in all shapes and sizes as scammers become increasingly sophisticated. Whilst the Government’s ban on cold calling is welcome it is only part of the solution.

“There are other steps the Government can also take to help protect people’s hard-earned savings. The PLSA is calling on the Government to make urgent progress towards introducing an authorisation regime for pension schemes. That will reassure people that they are only dealing with legitimate providers.”

-ENDS-

TABLE 1

TABLE 2

METHODOLOGY

The PLSA survey was an omnibus poll run by Opinium from 28 December 2017 to 2 January 2018 containing 2,004 nationally representative UK adults (aged 18+).

* = Based on PLSA survey respondents who failed to choose any of the following statements as possible pension scams: “When you are contacted by someone who is trying to get you to transfer your pension to an investment or scheme which seems too good to be true”; “When you speak to an adviser who tells you to take actions which you find out are not in your best interest”; “When you are advised to invest your pension fund into an investment that means you end up paying a huge tax bill”.

** = Calculated based on ONS population estimates.

*** = The Government’s response to the Work and Pensions Select Committee’s third report of session 2017-19 (Protecting pensions against scams: priorities for the Financial Guidance and Claims Bill), published 12 February 2018.

**** = Figures may not add up to 100% due to rounding

PRESS CONTACTS

Lee Blackwell, Head of Media and PR, Pensions and Lifetime Savings Association

T: 020 7601 1726, M: 07713 073023, E: [email protected]

Kathryn Mortimer, Press Officer, Pensions and Lifetime Savings Association

T: 020 7601 1748, M: 07901 007713, E: [email protected]

Eleanor Carric, PR Manager, Pensions and Lifetime Savings Association

T: 020 7601 1718, M: 07825 171 446, E: [email protected]